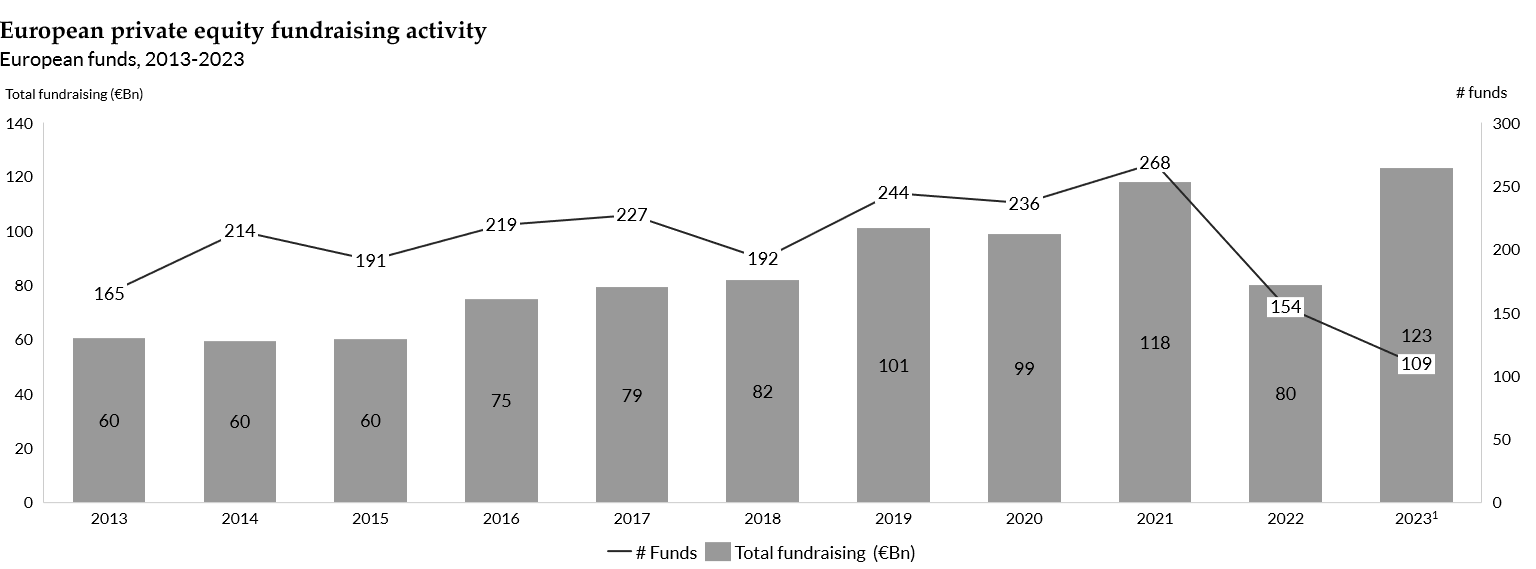

Following a funding slowdown in 2022, there has been a noteworthy resurgence, with European private equity funds projected to reach a historic high of €123 billion of capital raised during 2023.

This increase in fundraising has been more concentrated, with a lower number of funds closed in 2023 compared to previous years, while driving the total fundraising value upward. Notably, the top three funds account for 44% of total funding and account for a significant portion of total securities.

Despite the increase in available capital levels, there has been a substantial decline in leveraged buyouts activity (leveraged buyouts) throughout 2023. It is expected that the number of transactions and their value will decrease by around 20% and 30% annually, respectively, compared to the values of 2022, indicating a slowdown in activity during the year.

This downturn can be attributed to the significant rise in interest rates, which are making LBO financing more expensive. Consequently, this has elevated the return thresholds required for the realisation of an LBO transaction, ultimately leading to a reduction in the number of LBO operations which are materialised.

The recent contraction in deal volumes has resulted in a significant compression of transaction multiples, dropping from an average of c.11x in 2021 to c.9x in in the third quarter of 2023. The reduction in transaction multiples is making private equity firms reticent to sell their portfolio assets, as they have a higher difficulty in hitting return thresholds without the multiple expansion forecasted.

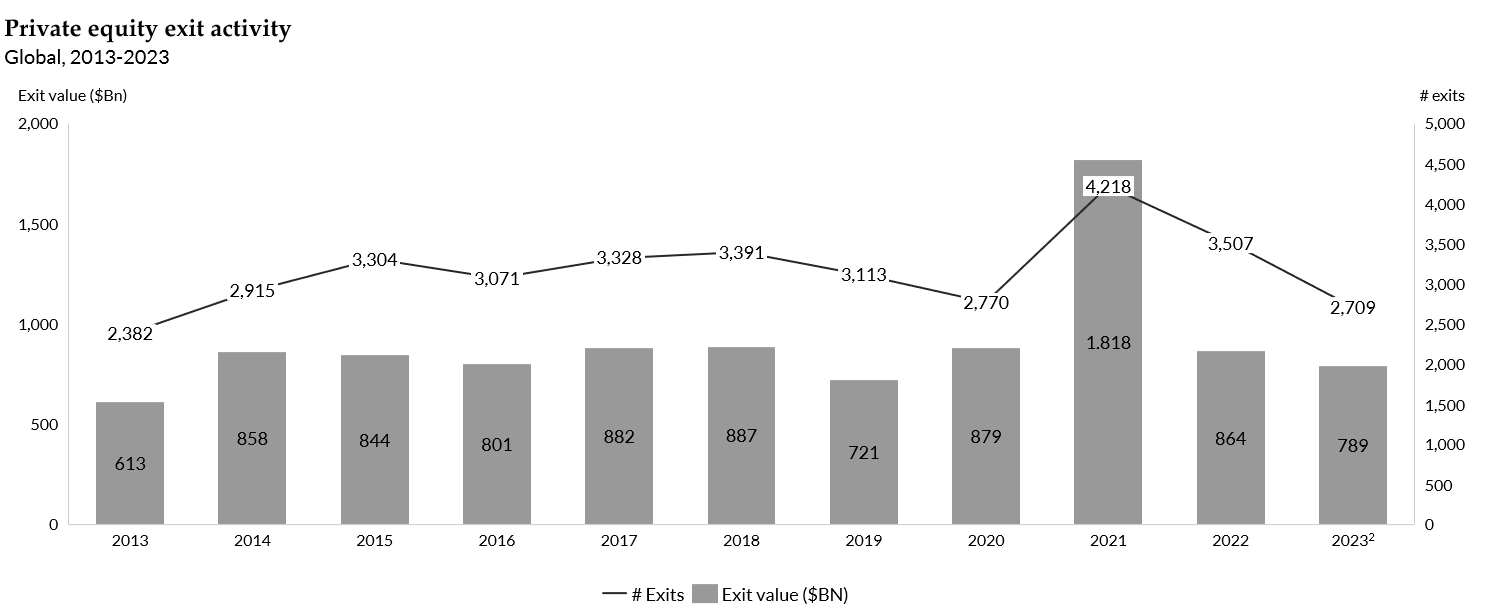

Consequently, an increasing number of firms are opting to extend their holding periods. This strategic shift has translated into a notable reduction in exit activity for the year 2023, with anticipated declines of around 20% in volumes and approximately 10% in value compared to the levels recorded in 2022.

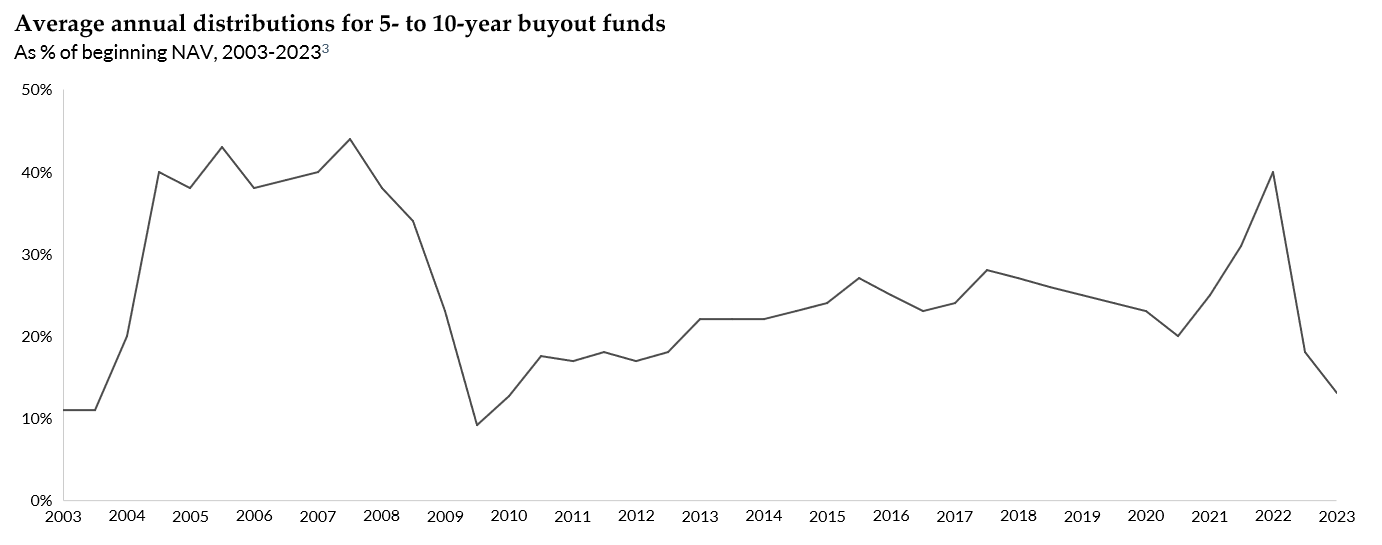

The decrease in exit activity is reducing the ability of venture capital firms to distribute funds to their investors, resulting in a decrease in fund distribution ratios. Consequently, the average annual distributions of buyout funds with a vintage between 5 and 10 years have experienced a notable decline.

Since the recent high reached in Q4 2021, where distributions reached c.39% of the fund’s Net Asset Value (NAV) at the beginning of the year (hereinafter initial NAV), the figures have dropped to c.13% of NAV initial starting in Q2 2023, significantly impacted by the delay in exits caused by a reduction in average transaction multiples. This is the lowest figure recorded since the lows of 9,2% in the fourth quarter of 2009 and 12,7% in the first quarter of 2010.

The current macroeconomic landscape, which discourages exits and has been slowing down distributions, is fostering the proliferation of fund financing solutions like NAV loans, which are increasingly being used by private equity firms to continue funding companies ahead of a sale in a more favourable market condition. NAV loans enable private equity firms to extend their holding periods effectively and serve as a source of additional capital, which can be used to fund value creation strategies or add-ons, in preparation for a short-term exit.

This market dynamic has been less adverse in the lower mid-market4, the space in which Qualitas Funds invests par excellence. According to Pitchbook, the proportion of total operations private equity corresponding to this market has increased, as smaller companies tend to use a lower proportion of debt to generate returns and, as such, are partially insulated from market conditions. In contrast, the proportion of total transaction value corresponding to transactions of more than €1.000 billion has decreased from 25% in 2022 to 17% in 2023.

This increased trading and exit activity in the lower mid-market has resulted in larger distributions for investors, higher than those seen in larger funds. On average, venture capital funds in the lower mid-market whose start year falls between 2016-2018 have an IPR of c.67%, compared to c.57% for larger funds5.

Looking ahead, interest rates are expected to decline as inflation slows and reaches its target levels. The FED has signaled its intention to carry out three interest rate cuts in 2024, and expects to implement further cuts in 2025 and 20266. The European Central Bank (ECB) also plans to start implementing interest rate cuts in 2024. The drop in interest rates is expected to result in an increase in the number of LBO transactions. Following the record year of fundraising, investors have a large amount of payable capital, and are expected to rapidly increase the pace of investment once macroeconomic conditions improve.

It is anticipated that the lower mid-market have more tailwind in the future, as it will benefit from increased catchment in the upper levels of the private equity, which cascades down to the lower levels. This happens because “mega funds” often acquire fund companies that operate in the lower mid-market, transferring capital to this segment through the acquisition of companies. Therefore, the increase in available capital at the top end of the market is expected to help boost returns in the lower mid-market In the near future.

Notes

Note 1: 2023 data has been annualised; annualised data is based on data up to November 2023. Sourced from Pitchbook.

Note 2: 2023 data has been annualised; annualised data is based on data up to September 2023. Sourced from Pitchbook.

Note 3: 2023 data is up to June 2023. Sourced from Pitchbook.

Note 4: Lower Mid-Market (LMM) funds are defined as those whose fund size is smaller than $1 BN.

Note 5: Analysis done by Qualitas Funds. Data sourced from Preqin; excludes Venture Capital (VC) funds, co-investment funds and Funds of Funds (FoF) among other categories.

Note 6: Sourced from Reuters and US News.