However, the extent to which it provides a strong predictor of this future performance materialising is limited, and a much wider array of factors must be considered for fund selection.

In this article we analyse how this return persistency changes with fund size and with the degree of size increase compared to the previous fund.

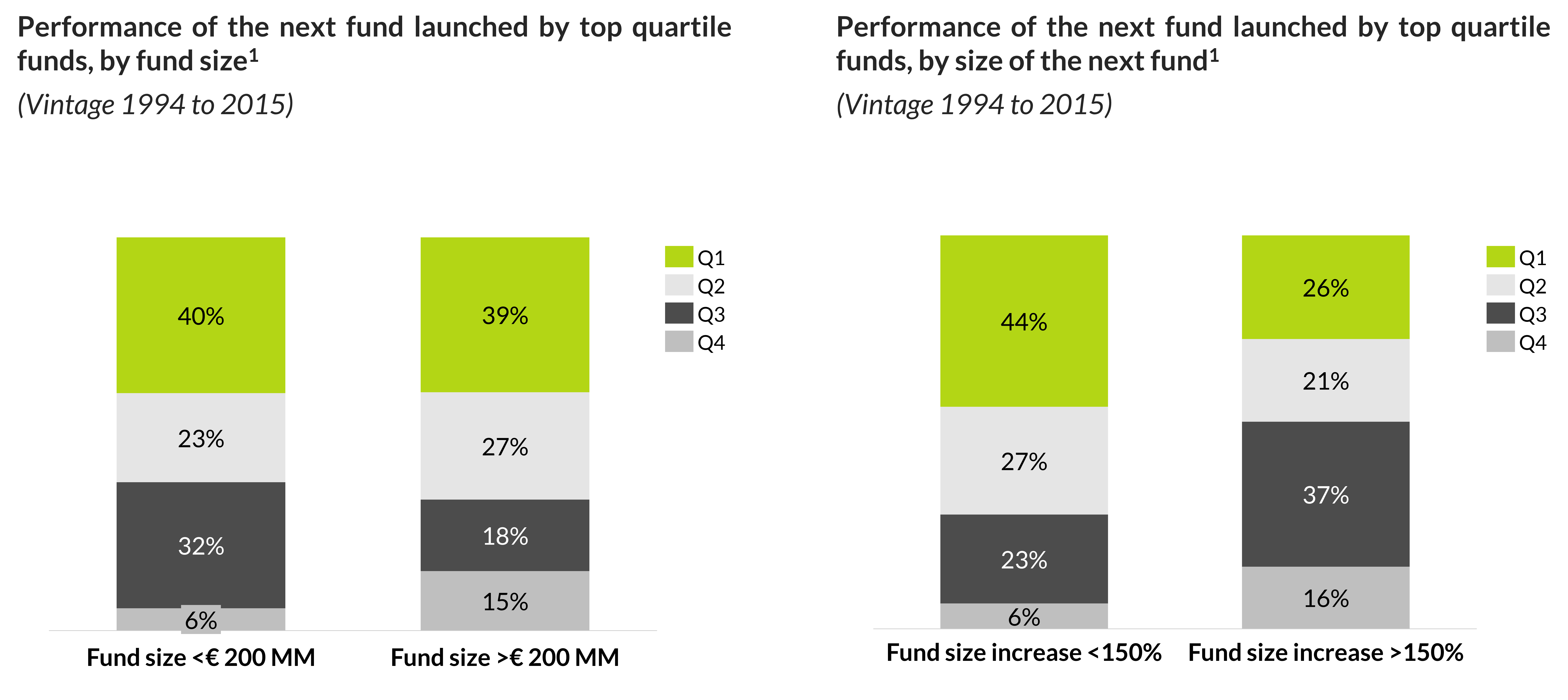

In the European LMM, predictability remains consistent across various fund sizes. Our analysis shows that approximately 40% of successor funds of top quartile performers with fund sizes under €200 million maintain their top quartile status in their next fund. Similarly, 39% of successor funds with fund sizes exceeding €200 million also maintain their top quartile status. This indicates a minimal difference in predictability based on fund size.

Nonetheless, a notable disparity in predictability emerges when considering the magnitude of fund size increases in subsequent launches, using the percentage increase from fund N to fund N+1 rather than the absolute fund size.

Around 44% of successor funds to top quartile performers with fund size increases below 150% maintain their top quartile status. In contrast, only 26% of successor funds to funds with size increases exceeding 150%, demonstrate top-quartile performance. Moreover, less than half of the funds achieved above average performance, indicating a substantial decrease in predictability of returns.

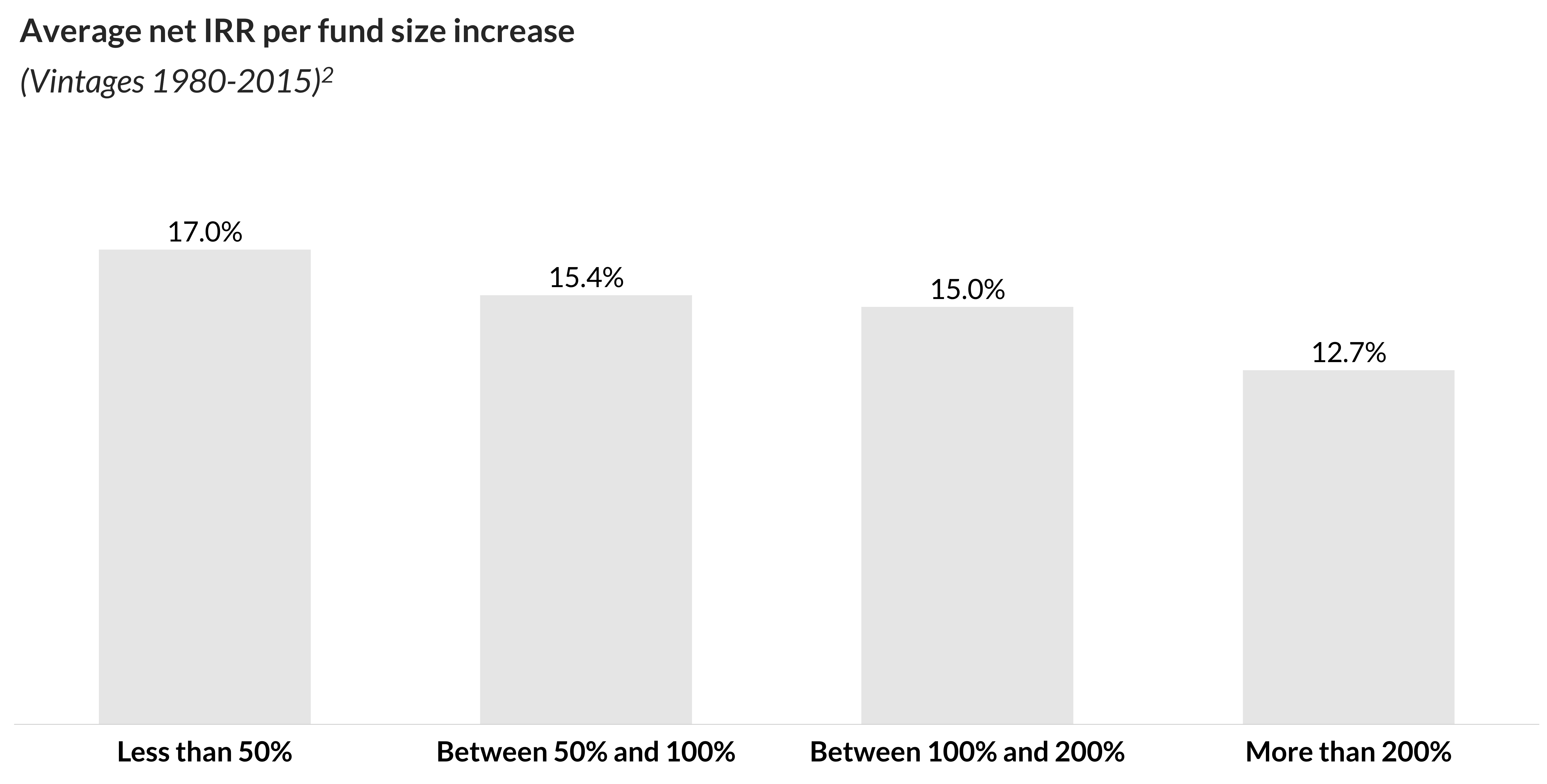

This phenomenon can be attributed to a decrease in returns, as the size of the next fund experiences a larger increase. Among the broader range of European funds, those with fund size increases of less than 50% exhibit an average net IRR of 17%. In contrast, funds with fund size increases ranging from 100% to 200% show an average net IRR of approximately 15%, while those with more than a 200% fund size increase demonstrate an average net IRR of around 13%.

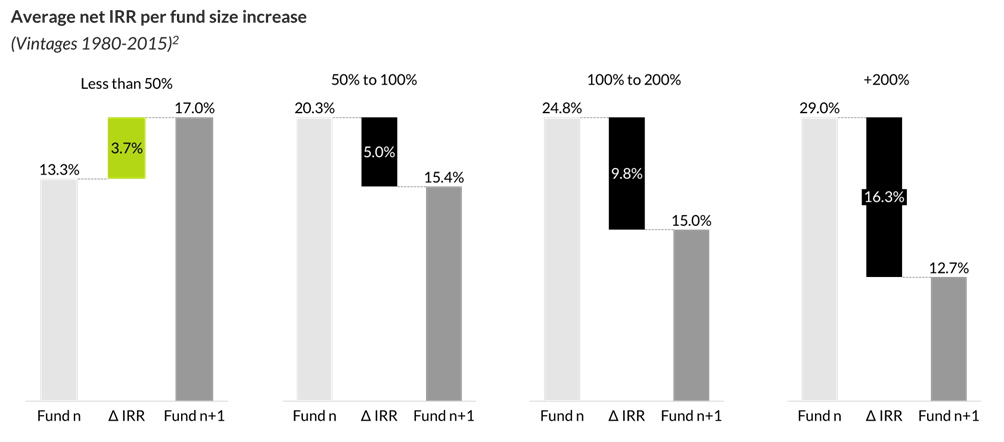

Anecdotally, funds with substantial increases in fund size have often had exceptional past performance. This success enables them to attract more capital from investors, leading them to pursue larger deals that may lie beyond their original investment focus. Consequently, these funds may transition away from their core investment thesis, venturing into larger markets and departing from their initial strategy. This shift tends to negatively impact the returns of their subsequent funds compared to the previous ones.

This phenomenon is observed across all fund size increases exceeding 50%, with varying degrees of impact on returns. Funds experiencing a fund size increase of 50% to 100% typically encounter a 5-percentage point (pp) drop in returns. Remarkably, this drop in returns escalates to c.16 pp for funds with larger fund size increases. Notably, only funds with a fund size increase of less than 50% demonstrate an increase in returns, with returns rising by approximately 4 pp.

We can conclude that the repeatability of returns at the top end of the spectrum is not influenced by the initial fund size but rather by the magnitude of the fund size increase in subsequent launches. Funds experiencing greater fund size increases tend to exhibit lower levels of repeatability in achieving top-end returns. This trend is attributed to GPs deviating from their investment thesis’ sweet spot as fund sizes increase, consequently leading to underperformance.

Stay tuned for our next publications where we will complement this analysis with how repeatability of returns changes with fund strategy.

Notes

Note 1: Sourced from Preqin and complemented with data from Qualitas Insight. Filtered to include private equity funds with a geographical focus in Europe, with fund sizes of less than € 1Bn and vintages before 2015. Quartiles are based on MoC and have been calculated using the analysis dataset and cross-referenced with third-party quartiles like Cambridge Associates.

Note 2: Qualitas Funds analysis based on Preqin data of funds with an investment presence in Europe and vintages before 2015. N=1,171.