This concept holds particular significance for us at Qualitas Funds as we strive to consistently identify and invest in top-tier European lower mid-market private equity funds and foster enduring partnerships with premier GPs in this dynamic market landscape.

By harnessing third-party databases alongside our proprietary Qualitas Insight platform, we’ve conducted a comprehensive analysis focusing on the persistence of funds within the European mid-market landscape. Our findings indicate that while the past performance of private equity funds can offer some insights into their potential future performance, fund selection must be more nuanced and take into account other factors. The success of a top-performing fund does not inherently guarantee positive performance for its successor, highlighting the multifaceted nature of fund selection.

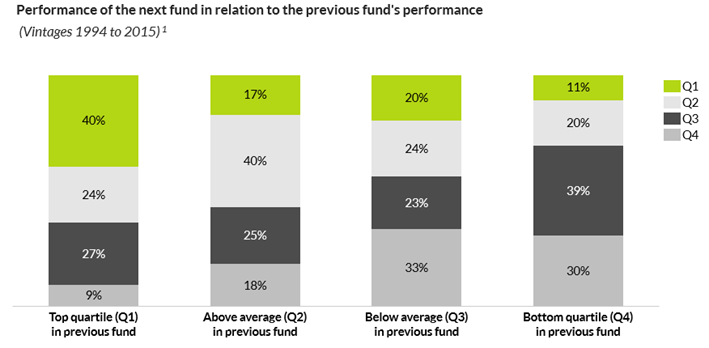

Based on our analysis, c.40% of successor funds to top quartile performers maintain their top quartile status in their next fund, while approximately two-thirds of top quartile funds yield funds that outperform the average. Additionally, a mere 9% of top-quartile funds generate successors that fall into the bottom quartile, further highlighting that past performance is a somewhat statistically significant variable in terms of future fund returns.

The statistical significance of past performance is also evident at the lower end of the return spectrum. Approximately 30% of successors to bottom quartile funds remain in the bottom quartile, while over two-thirds land in the bottom half, and only about 11% ascend into the top quartile.

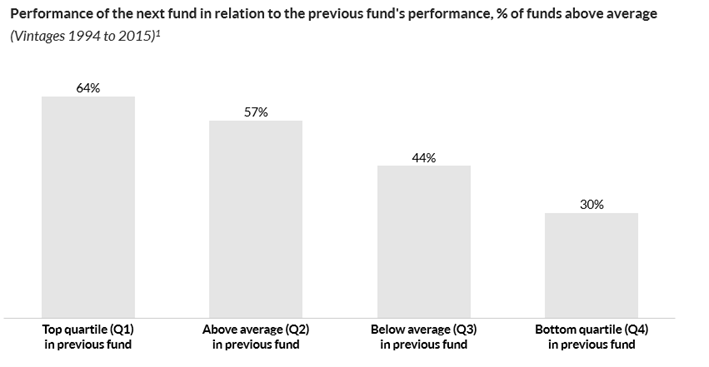

Interestingly, the percentage of non-top quartile funds whose subsequent fund achieves top quartile status remains relatively consistent across above-average, below-average, and bottom quartile funds, at the 10-20% range. However, when examining the occurrence of funds yielding above-average performance, we observe a more pronounced correlation with the performance of their previous fund.

Hence, we can conclude that past private equity performance can somewhat serve as an initial indicator of future fund returns, but the extent to which it provides a guarantee of this future performance materialising is limited. To truly guarantee the persistence of returns, it is important to go one step deeper and consider a wide variety of other factors.

In the following editions of our monthly newsletter, we will aim to differentiate how the degree of repeatability of funds with different characteristics varies and analyse what are the features that consecutive top-quartile funds have in common, to ultimately unpack the degree to which and reasons why the best GPs can deliver top-quartile performance across many of their funds.

We will also analyse the shift in fund strategy and changes in characteristics of funds that rise to the top quartile from below-average performance and those that drop to bottom quartile performance from better-than-average performance.

Notes

Note 1: Sourced from Preqin and complemented with data from Qualitas insights. Filtered to include private equity funds which have a geographical focus in Europe, fund sizes of less than € 1 BN and vintages from 1994 to 2015. Quartiles are based on MoC and have been calculated using the analysis dataset and cross-referenced with third-party quartiles like Cambridge Associates