Deal-by-deal managers are private equity managers who operate independently, assessing and executing each investment individually without grouping their investments and enclosing them in a traditional fund structure. Unlike conventional private equity funds, these managers do not raise and deploy capital in fund structures, but seek funding for specific transactions. They tend to have a smaller pool of capital from which to invest and have smaller team sizes than traditional funds. As such, they typically invest in smaller-sized companies, have a slower deployment pace, and smaller portfolios.

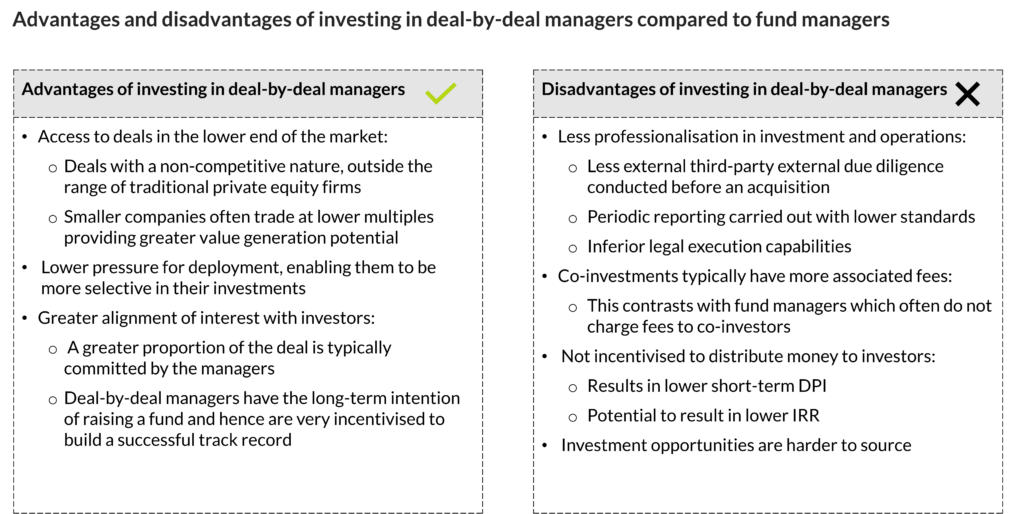

Investing in deal-by-deal managers brings a series of advantages compared to investing in traditional funds. Deal-by-deal managers often target companies which are smaller in scale in both revenues and EBITDA and hence often fall below the size scope for traditional fund managers, who normally cannot have access to those deals. As a result, they usually take part in less competitive processes, leading to effectively cheaper entry multiples on their deals, providing downside protection and greater value generation potential.

Also, since deal-by-deal managers do not invest from a traditional fund structure with a fixed investment period duration, they have no pressure to deploy capital, hence they can “cherry-pick” their deals and only invest in the best opportunities they identify. The fact that they have smaller companies’ portfolios also allows them to dedicate more time and attention to each portfolio company, helping them successfully complete value creation and transformational initiatives.

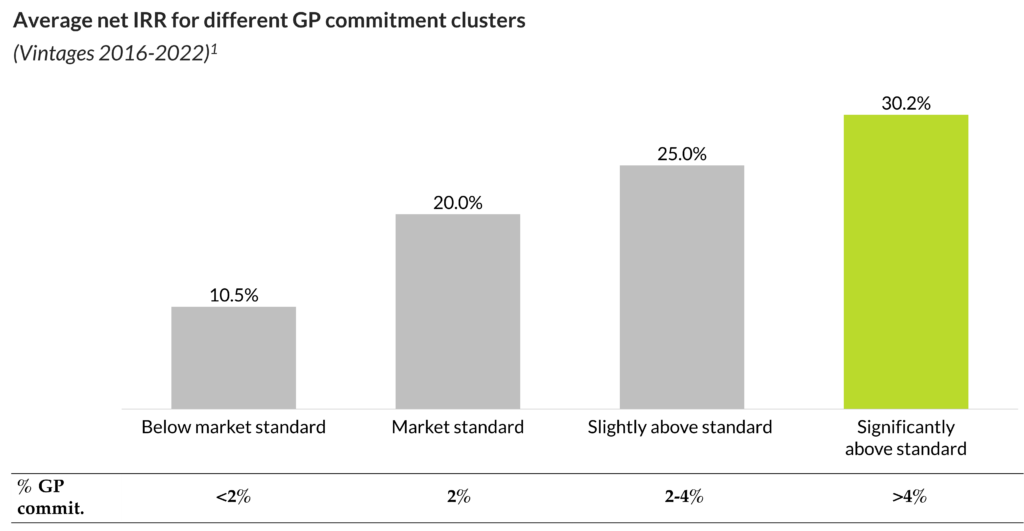

Additionally, deal-by-deal managers commit a larger proportion of their own capital into their investments, and often have the objective of later raising a fund, thus, investing in deal-by-deal managers provides a greater alignment of interest with the GPs. As shown in the below chart, funds with higher GP commitment have higher average net IRR, indicating that greater alignment of interests typically leads to higher returns.

However, investing with deal-by-deal managers brings a series of disadvantages with respect to traditional fund investments. For example, the level of professionalisation of their investment and operational activities is typically lower than that of traditional fund investors. This typically manifests in lower levels of third-party external due diligence carried out before closing each deal, less detailed business plan models, lower legal execution capabilities, and inferior reporting and quarterly updating capabilities.

Also, since they are not part of a fund structure with a fixed timeline, they might have lower incentives to exit their investments if the companies are performing well, hence, investing in these companies might result in comparatively longer holding periods when compared to traditional co-investments in fund portfolio companies, sometimes penalising the investor’s IRR. Additionally, virtually all co-investments with deal-by-deal managers have some degree of fees associated with their activity, whereas co-investments in primary funds in which the GP is already an investor typically have no fees and no carried interest associated with them.

Finally, these types of investment opportunities are very hard for fund of funds managers to source, as they require very deep market coverage and contact networks, making it harder for them to access high-quality deal-by-deal opportunities.

To summarise, investing with deal-by-deal managers has the potential to be very lucrative, as they target companies in the smaller end of the market and seldom compete for deals, hence they can buy companies cheaper, and they have a higher level of alignment of interests than traditional fund investors, which is a premise for superior returns. However, these investments have some associated risks, including a lower level of professionalisation in investments and operations, lower incentives to exit assets, and fees associated with each co-investment. Thus in order to reap the benefits of carrying out a deal with these managers, it is important to be able to mitigate the identified risks.

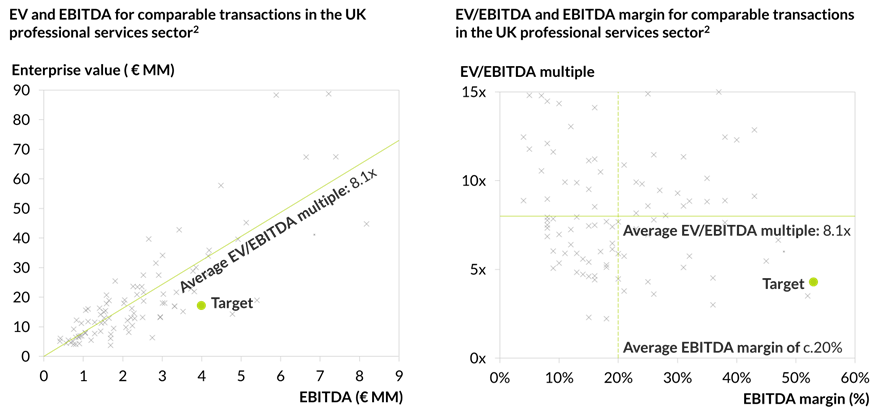

In Qualitas Funds, we have recently carried out a co-investment with a deal-by-deal manager from the UK. The manager offered us the opportunity to co-invest in a company with c.50% EBITDA margins, high cash conversion rates and revenues growing at c.40% per annum. The GP identified this company through their connection with a small regional advisor, spent time building a relationship with the company management and positioned themselves as their preferred partner. They secured the transaction at a strong discount compared to market multiples, paying a multiple of c.4.2x EV/EBITDA compared to the sector average of c.8x EBITDA. The Qualitas Funds’ team found this deal attractive, as it involved purchasing a majority stake in a high-quality asset at a relatively cheap valuation, and carried out extensive due diligence to make sure that the risks associated with investing in a deal-by-deal manager were mitigated in this operation.

Particularly, the deal-making and operational capabilities of the team were verified via an extensive referencing exercise and thorough background checks. We found that the team members had valuable experience and successful careers in investing. This was exemplified by the manager’s previous track record and their recent first exit generating a gross return of >10x MoC. The team included operational and legal partners, to ensure that the GP had fund manager-level operational, legal and reporting capabilities.

Before signing the deal, the deal-by-deal manager team carried out extensive due diligence on the asset they were investing in, performing political, commercial, technical, technological and financial due diligence, and employing external advisors to assist them. This allowed them to have a holistic and deep knowledge of the asset and its underlying market, which, upon contrasting with our own due diligence, gave us comfort in the underlying fundamentals behind investing in the asset.

Finally, the manager is incentivised to eventually exit the company by keeping their management fee to 0% and implementing a carried waterfall structure also dependent on the investment’s IRR, rather than solely by MoC. This ensures the manager is properly incentivised to exit the company within a reasonable holding period and distribute money to investors.

In conclusion, we believe that selectively co-investing with deal-by-deal managers can be positive for the return profile of a fund of funds portfolio if done properly. Fund of funds should only invest in this type of deals if the investment case mitigates the risks inherent in investing with these managers. They must make sure that the deal-by-deal manager has a professional operation in place and carries out appropriate levels of due diligence before deal execution. Additionally, they must make sure that there is a good alignment of interest between the deal-by-deal manager and the fund of funds, evidenced by a high commitment from the deal-by-deal team, a strong link between management fees and returns, and an underlying intention to develop the firm. Only in the situation that these premises occur and the team concludes that the deal is an attractive investment opportunity after due diligence, fund of funds managers may consider investing in these deals.

Notes

Note 1: Qualitas Funds’ analysis based on data from Qualitas Insight, funds with vintages from 2016 to 2022 (N=60). Funds at various stages of maturity, with both unrealised and realised components.

Note 2: Average transaction multiples from professional services companies in the UK with € 5-20 MM in sales. Source: Qualitas Insight.