This has led to an EV/EBITDA transaction multiple compression, from a c.11.6x average EV/EBITDA multiple in 2021 to a c.9.1x average EV/EBITDA multiple towards the end of 20232.

In Q1 2024, the trend has continued and deal volumes have decreased by c.19% compared to Q1 2023, thus, transaction multiples have not picked up3. Hence, private equity firms are struggling to exit their portfolio companies at sufficiently attractive prices and are often opting to extend the life of their investments. To do so without compromising the rate of return of the investments, they are engaging in value-generating activities to continue driving returns. One such activity is the acquisition of add-on companies to drive synergies and realize value through multiple uptick.

General Partners (“GPs”) are increasingly using fund-level credit, in the form of NAV lending, to fund these add-ons. This is evidenced by the fact that lenders providing these types of loans have seen an increase in lending volumes used to fund add-on acquisitions. Rede Partners has reported that in 2023 and 2024, around 55% and 82% of lenders respectively have seen an increase in NAV loan deal volume to fund these types of transactions.

It has been seen that using NAV financing to finance these transactions helps fund managers increase their returns while resulting in limited risk for their investors. To illustrate this, we present a case study explaining how a fund can use NAV financing to fund add-ons for portfolio companies and strengthen its market position.

Consider a fund that has used 90-95% of its capital to acquire 8 portfolio companies, with the remainder reserved for fee payments and investments in other assets. One of the fund’s 8 platforms is struggling to meet its initial business objectives, hence the return expectations for these assets have gradually fallen below original return expectations. Several years into the holding, the management team came across the possibility of acquiring an add-on that offered complementary products to the existing offering of the initial platform and was expected to generate significant synergies upon integration. The add-on is smaller in size than the portfolio company and was trading at a discount in terms of EV/EBITDA multiple, so its acquisition would also contribute to enhanced value generation via multiple uptick when integrated with the platform company.

After the acquisition, it was predicted that the revenue growth rate would increase from 5% to 8% driven by increased cross-selling, and the EBITDA margin would increase from 10% to 12% driven by fixed cost rationalisation. This EBITDA expansion, alongside the assumed multiple uptick and debt repayments, is predicted to generate a gross return to investors of 2.5x-3.0x MoC, depending on the solution used to fund the transaction.

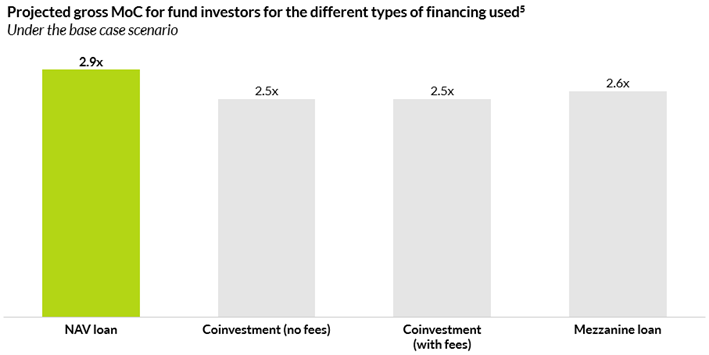

Due to the attractive return perspectives, the fund is determined to realise this add-on, but it has no dry powder left for investments from the fund. Hence it is considering either offering co-investments to new or existing Limited Partners (“LPs”) or obtaining mezzanine financing or NAV financing. Assuming that the company behaves as predicted by the base case business plan, using an NAV loan would result in a gross MoC of c.2.9x for fund investors, which is superior to the gross returns generated when using co-investments and mezzanine type financing, which would result in gross returns of c.2.5x MoC and c.2.6x MoC, respectively.

NAV financing generates superior returns than co-investments, as it avoids the dilution of fund investors in this opportunity. The cost of capital of NAV lending is c.10-12%, which is smaller than the c.15-20% IRR of the opportunity, thus the use of NAV lending is value accretive, as its cost of capital is significantly below the projected return of the opportunity. Using NAV lending also allows GPs to find financing for deals where it would not be so attractive to be a co-investor. For this deal, investors would obtain a gross MoC of c.1.9x in the base case, which may be below their threshold for investing, and hence GPs may find it hard to find investors with appetite for this opportunity. Additionally, NAV financing allows GPs to be able to fund multiple opportunities at a time with one single process, in case it wants to finance add-ons for multiple platforms. This strategy benefits GPs by providing a single source of capital for all these transactions, which is more efficient than seeking multiple sources of funding.

On the other hand, the interest rate terms of NAV loans (c.10-12%) are more favourable than the typical 15-20% “all-in” rates associated with mezzanine financing, leading to a better return profile for the sponsor. Additionally, mezzanine loans include company-level covenants that restrict the portfolio company’s operations, whereas NAV loans have covenants at the fund level, avoiding this issue. Furthermore, the execution speed of NAV financing is faster than mezzanine lending, allowing sponsors quicker access to financing. All the above reasons make NAV lending more advantageous than obtaining mezzanine loans in most cases.

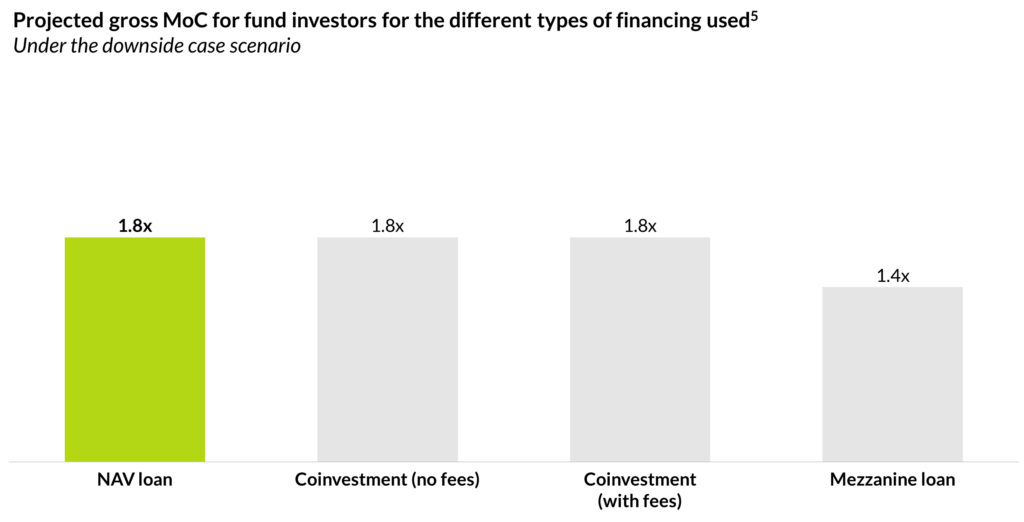

NAV financing also shows superior returns in the case where the company does not perform according to the business plan. Consider that following the acquisition, the company’s revenue growth rate decreases from 5% to 4.5% and the EBITDA margin stays constant. Under this scenario, the return for fund investors from using co-investment and NAV lending is c.1.8x gross MoC, whereas the return for fund investors when using mezzanine lending is c.1.4x gross MoC. In addition, the return for co-investors would be c.1.4x under this scenario, which is much smaller than their target returns. This implies that NAV lending is the most optimal financing methodology for a wide range of scenarios.

As a result of its favourable return characteristics and increased flexibility in comparison to other alternatives, LPs tend to have a favourable view of the use of NAV lending facilities to fund add-on acquisitions. According to the Rede Partners survey, 86% of investors view these solutions positively or have a neutral attitude towards NAV loans used to fund add-on acquisitions. Communication is the most common key concern from LPs, with 31% of LPs ranking it as their key concern. Therefore, to bring LPs on board, fund managers need to improve transparency and communication. If the use of proceeds is compelling and the opportunity is well communicated to LPs, they tend to be supportive in implementing these solutions.

In conclusion, funding add-on acquisitions using NAV financing can be a suitable solution to extend the life of assets and avoid selling them at a lower price due to the current adverse environment for exits. NAV lending is competitive compared to co-investments and mezzanine loans, both in terms of rates and flexibility, often resulting in superior returns for fund investors, even when considering downside cases. Finally, this type of transaction is gaining recognition among LPs as a good solution for funding add-on acquisitions and fostering the portfolio companies’ value creation.

Notes

Note 1: Sourced from Pitchbook. Data for 2023 was annualised based on data up to September.

Note 2: Sourced from the Argos index, which tracks the evolution of the historic EV/EBITDA multiples for mid-market companies, under a 6-month rolling basis.

Note 3: Sourced from Q1 2024 European PE Breakdown report from Pitchbook.

Note 4: Sourced from Rede Partners report “NAVigating NAV Financing: LP perception survey and lender market report”.

Note 5: Analysis carried out by Qualitas Funds based on an illustrative case study.