GPs (General Partners or Sponsors) can also use other types of financing solutions like management company loans to create value for their investors (Limited Partners or LPs).

Management company loans offer GPs a flexible and tailored solution to address strategic capital needs, whether for growth opportunities or managing transitional periods, by taking as collateral a claim over future management company cash flows. These loans provide GPs with the financial resources to scale their operations, seize opportunities, and ensure continuity during transitionary periods.

When it comes to funding growth opportunities, management company loans are an attractive solution for sponsors who are in the process of growing their platform but have insufficient capital to support this expansion. A common use case is enabling GPs to increase their commitments to subsequent funds, aligning their interests with LPs. Additionally, GPs can use these loans to seed capital for launching new strategies or expanding into new geographies, allowing them to diversify their product offering. They can also be used to support the recruitment of new personnel, ensuring the firm is well-resourced to manage its growth, or facilitate the buyout of existing management company investors, giving GPs greater control over the strategic direction of their platform.

In transitional periods, management company loans can provide support for GPs to manage these complex scenarios. For instance, these loans can be used to finance the acquisition and warehousing of deals, allowing GPs to secure attractive opportunities even before a new fund is launched. Management company loans can also be used to bridge funding gaps during GP stake sales or to finance equity participation for junior team members, supporting a smooth transition in management succession planning.

Management company loans can take a diverse range of collateral assets, making them a highly viable solution for sponsors with imminent capital needs that need to fund these types of applications. Management fees tend to be the most common collateral and are valued based on the net management company cash flows before partner compensation. Another important collateral can be the carried interest of the platform, which is valued based on the current carry from existing funds and discounted based on fund strategy, performance and DPI. Additionally, other collateral assets may be considered in situations where more diversity or value is required.

To further exemplify the usefulness of these solutions, we present 2 studies regarding the funding of additional GP commitments as well as the warehousing of a deal.

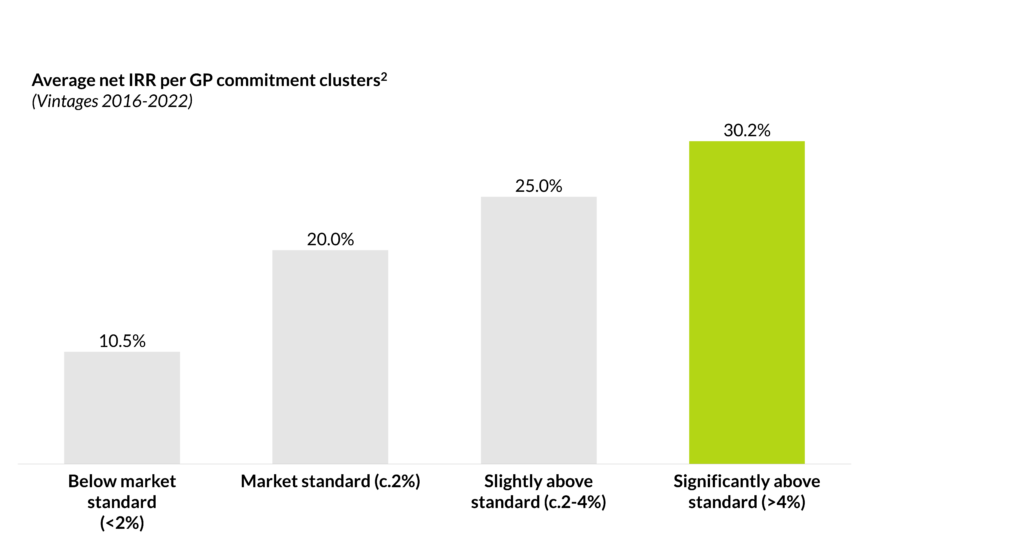

Financing GP commitments can create value for LPs by enhancing the predictability of fund-level returns. Following industry standards, the average manager’s contribution is typically around 2%¹. By contributing their own capital to the fund, the manager provides a clear statement of intent and implicitly commits to seeking satisfactory returns. This will generate a higher level of trust among potential investors, who see how their incentives and those of the manager are aligned. Management company loans can allow GPs to increase their commitments to subsequent funds strengthening this alignment between GPs and LPs.

As reflected above, funds in which the management team commit less than 2% of the fund size (below the market standard) performed worse than those in which the team contributed a higher percentage, achieving a c.11% net IRR. Funds, where managers committed c.2% of the fund size, achieved an average net IRR of 20%, while those that contributed more than 4% achieved an average return of 30%. The data highlights the clear relationship between the fund’s GP commitments and the returns obtained by them. By providing capital to fund GP commitments, management company loans can enhance the alignment of interests between both GPs and LPs and thus, increase the predictability of achieving higher returns.

Furthermore, management company loans can also create value for LPs by providing capital solutions for GPs to manage transitions in the platform. Management company loans can be used to warehouse a deal for a new fund which can assist in mitigating the J-curve effect, making the fund more attractive to investors. This can be crucial in helping GPs fundraise their funds in the current macroeconomic environment.

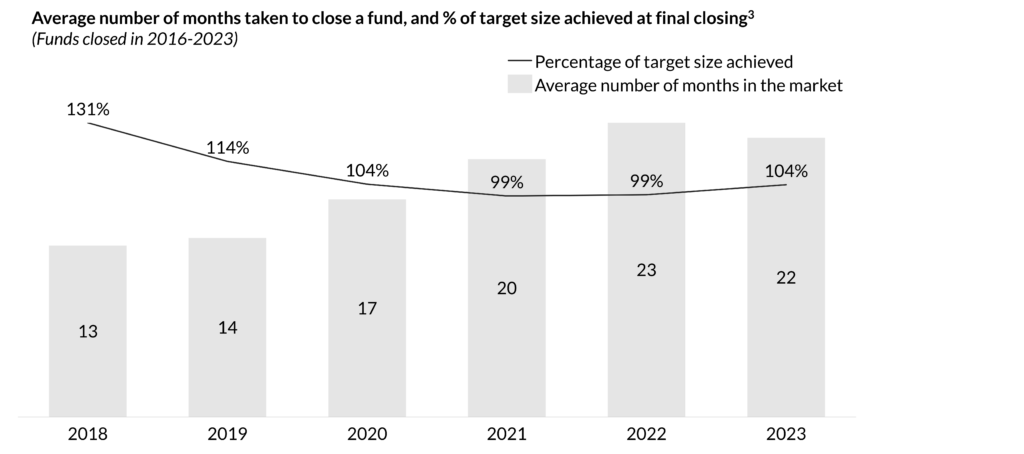

The fundraising landscape for funds has become increasingly challenging over the past few years. The average time to close a fund has risen significantly, from 3 months in 2018 to 22 months in 2023, reflecting a c.70% increase. At the same time, the average percentage of target size achieved by funds has decreased by 27 percentage points. These trends underline the need for sponsors to present more attractive offerings to investors to accelerate and achieve their fundraising activities.

Management company loans offer a strategic solution to address these challenges. By utilising these loans to acquire and warehouse assets for subsequent funds, GPs can remain active in the market, even in the absence of an active fund. This capability allows them to capitalise on high-quality deals as they emerge, ensuring that valuable opportunities are not lost. Additionally, this approach enables sponsors to acquire these opportunities at the cost of debt, which can later be transferred into the fund at market value.

For investors, such seeded portfolios are also highly appealing. They provide greater visibility into the fund, potentially accelerate distributions, and help mitigate the typical J-curve effect. By holding assets before the fund’s launch, sponsors create a more immediate return profile, making the fund a more attractive investment opportunity for investors and accelerating the fundraising process.

These studies highlight the viability of management company loans, which can be used to fund multiple types of growth opportunities and help GPs manage transition more effectively. This type of use cases makes them highly attractive not only for GPs but also for LPs resulting in the high appetite from managers and investors in using these solutions.

Hark Capital, part of US-based P10, with over $1.6 billion in capital deployed, has been a leading provider of fund financing solutions and management company loans in the US market since 2013, having successfully closed over 130 deals. Building on this track record, the firm is now expanding into the European market to meet the increasing demand for these financing solutions.

As part of this initiative, Qualitas Funds has successfully launched its new fund financing investment vehicle, Qualitas Continuation Finance I, in partnership with Hark Capital. This collaboration aims to deliver tailored, flexible, and non-dilutive financing solutions to European lower-middle market sponsors. The focus is on providing value-accretive solutions that align with the interests of LPs, covering multiple stages of the fund lifecycle through a variety of financing structures.

Through this partnership, Qualitas Funds and Hark Capital are well-positioned to meet the needs of the European market, bringing proven expertise and unparalleled execution experience in fund financing.

Notes

Note 1: CMS 2021.

Note 2: Qualitas Funds’ analysis based on data from Qualitas Insight, funds with vintages from 2016 to 2022 (N=60). The analysis was performed with funds at various stages of maturity, with both unrealised and realised components.

Note 3: Preqin. Dataset including European private equity funds which are closed to investment. N= 2,726.