As the graph shows, while total capital raised remained resilient through 2024, reaching €147Bn, the number of funds has declined sharply from its 2022 peak, and fundraising volumes fell materially in 2025 to €81Bn, underscoring a more uneven and uncertain fundraising environment for sponsors.

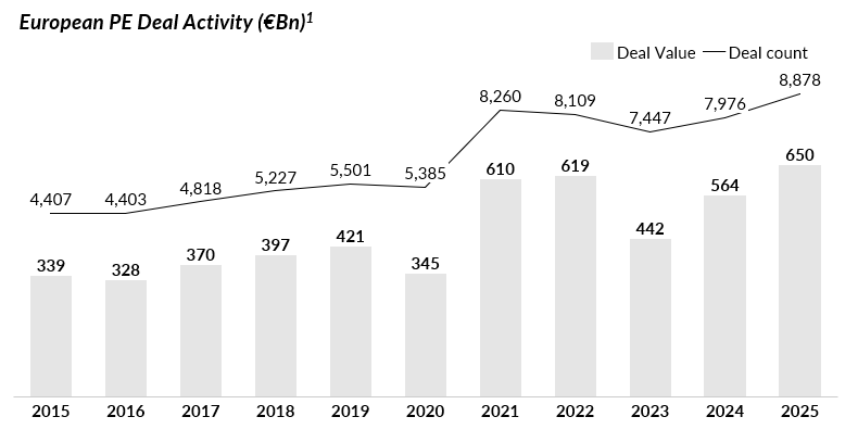

At the same time, deal activity across the European private equity market has remained robust. Following a temporary slowdown in 2023, both deal value and transaction volumes rebounded strongly in 2024 and 2025, with total deal value reaching €564Bn and €650Bn, respectively. This resilience in deal activity highlights a growing disconnect between the availability of capital at the fund level and the deployment pace.

For many sponsors, this imbalance between the pace of investment and the effective availability of capital creates a structural challenge during the early stages of a fund’s lifecycle. Delaying investments until a larger portion of commitments has been secured may result in missed opportunities, while calling significant amounts of capital too early can create unnecessary friction with investors and negatively affect fund dynamics.

In this context, fund-level financing solutions have continued to evolve to reflect the realities of the market. Beyond traditional facilities supported solely by uncalled commitments, or structures relying exclusively on portfolio value, hybrid solutions have emerged to provide greater flexibility while preserving alignment of interests between managers and investors.

Historically, fund-level financing has played a defined but relatively narrow role within private equity structures. Capital call facilities have long been used as short-term liquidity tools, allowing managers to bridge capital calls and manage cash flows efficiently during the investment period. More recently, NAV-based financing has emerged as a powerful solution for more mature portfolios, enabling sponsors to access liquidity supported by the value of their underlying assets and to address both offensive and defensive use cases at the fund level.

However, these two solutions tend to address opposite ends of the fund lifecycle. Capital call facilities are typically limited in size and duration, relying exclusively on uncalled commitments and designed to be repaid quickly. NAV financing, by contrast, requires a sufficiently seasoned portfolio with stable asset values and is therefore less suited to the earliest stages of a fund’s life, when net asset value is still in the process of being built.

Hybrid facilities across the fund lifecycle

Between these two extremes lies a phase that has historically been less well served by traditional financing structures. As illustrated above, this period is characterised by a gradual decline in dry powder alongside the early build-up of portfolio NAV, creating a natural overlap between commitment-backed and portfolio company backed sources of credit support. During this stage, funds may already be actively investing and executing on their strategy, while neither a short-dated capital call line nor an asset-backed NAV facility fully addresses their financing needs.

Hybrid loan structure

Hybrid facilities are designed precisely to address this gap. As illustrated in the lifecycle diagram above, by combining credit support from both uncalled commitments and the growing NAV of the portfolio, they provide sponsors with a flexible financing solution during the early stages of a fund’s lifecycle. This blended approach allows managers to access larger and longer-dated facilities than traditional capital call lines. It also helps them continue investing on their portfolio while fundraising, avoiding calling a large amount of capital from their first closers. This is done while maintaining a good credit risk profile, with a portion of liquid collateral from investor commitments that can be called upon covenant breaches and broader collateral coming from portfolio companies.

Importantly, hybrid facilities should not be viewed as a replacement for other forms of fund financing, but rather as part of a broader, sequential toolkit. As portfolios continue to develop and NAV becomes the primary source of credit strength, these structures can naturally transition into NAV-based financing, ensuring continuity and flexibility throughout the life of the fund.

Beyond their lifecycle positioning, the distinguishing feature of hybrid facilities lies in the way they combine commitment-backed and asset-backed credit support within a single fund-level structure. Unlike traditional capital call facilities, which rely exclusively on uncalled commitments and are typically short-dated in nature, hybrid facilities can remain outstanding for longer periods and scale alongside the growth of the portfolio. At the same time, unlike NAV-based loans, which require a sufficiently seasoned and stable asset base, hybrid facilities can be implemented at an earlier stage, when NAV alone would not yet support a fully asset-backed structure.

This dual-source approach allows hybrid facilities to bridge a transitional phase in the fund’s lifecycle that has historically been underserved by existing financing tools. By preserving flexibility in the early stages while maintaining discipline as asset-backed risk becomes more prominent, hybrid facilities enable sponsors to align financing structures more closely with the evolving needs of the fund. In many cases, the most immediate point of reference for sponsors considering a hybrid facility is the traditional capital call line. Capital call facilities remain well suited to short-term liquidity management and administrative efficiency. However, their reliance on uncalled commitments alone and their limited duration can constrain their usefulness in situations where sponsors require larger financing capacity, longer tenors, or greater certainty during periods of prolonged fundraising.

Hybrid facilities address these limitations by incorporating portfolio NAV alongside uncalled commitments as sources of credit support. This allows for greater financing capacity and increased structural flexibility, while maintaining a conservative, fund-level risk profile. As a result, capital call lines and hybrid facilities should be viewed as complementary tools rather than substitutes, each serving a distinct role within the broader fund financing toolkit.

A key distinction between hybrid facilities and traditional capital call lines lies in their covenant frameworks. Capital call lines are typically governed by commitment-based covenants, focused primarily on investor coverage ratios and concentration limits, and are designed to manage short-term liquidity risk. Hybrid facilities, by contrast, incorporate a broader covenant set that reflects their dual source of credit support. Alongside commitment-based protections, they introduce asset-based metrics such as loan-to-value limits, portfolio concentration thresholds and eligibility criteria as NAV builds. This evolving covenant structure allows leverage to scale in a controlled manner as the fund matures, preserving flexibility in the early stages while maintaining discipline as asset-backed risk becomes more prominent.

In an environment characterized by uneven fundraising dynamics and sustained deal activity, hybrid facilities have emerged as a valuable addition to the fund-financing toolkit. By combining commitment-backed and asset-backed credit support, these structures allow sponsors to navigate a critical phase of the fund lifecycle with greater flexibility, execution certainty and alignment with investors. When used prudently, hybrid facilities help bridge the gap between early-stage financing and more mature NAV-based solutions, supporting disciplined deployment without compromising long-term value creation.

Notes

Note 1: Sourced from Pitchbook’s European Private Equity 2025 report.