The expansion of the secondary market has been driven by both LP-led and GP-led activity. On the LP side, investors—including pensions, sovereign wealth funds, endowments, and asset managers—are increasingly using secondaries as a strategic tool, selling underlying fund positions to access liquidity. What was once primarily a liquidity-driven exercise has evolved into a proactive approach to rebalance exposures, reduce overallocation, and create flexibility for new commitments. This shift has made LP-led sales a regular feature of portfolio management, with buyout funds still dominating transaction volume, while credit, infrastructure, and venture markets are seeing rising activity.

Meanwhile, GP-led solutions have emerged as a central growth engine for the market. Continuation funds, once considered a niche structure, now account for nearly half of total secondary activity. These vehicles allow managers to retain their highest-quality companies beyond the traditional fund life, while providing liquidity options to existing investors and attracting new capital for growth initiatives. With target returns typically in the range of 2–3x MoC and 20–25% IRR, continuation funds offer a compelling mix of alignment and performance potential. In a muted M&A and IPO environment, GP-led secondaries have transitioned from a backstop to a mainstream exit route and a powerful liquidity solution. As a result, the GP-led market is expected to continue expanding even as traditional deal and exit activity rebounds.

The rise of LP-led and GP-led transactions has transformed the secondary market from a niche segment into a core pillar of private markets, driving record volumes and reshaping how investors approach liquidity and value creation. For investors, secondaries offer a compelling combination of liquidity, diversification, and attractive risk-adjusted returns. By acquiring interests in funds and companies that are already partway through their investment cycle, secondary buyers gain visibility into underlying portfolios and avoid the blind-pool risk. Transactions often occur at a discount to quoted net asset value, creating potential for built-in upside, while the shorter duration profile accelerates distributions and mitigates the J-curve effect. Meanwhile, continuation funds and other GP-led structures provide targeted access to proven, high-quality assets with strong growth potential and meaningful alignment with GPs.

It is worth noting that, as in the broader private equity market, the dynamics of the lower mid-market in secondaries differ from those in the “large cap” segment. Generally, the lower end of the secondary market faces less competition, which often translates into more favourable pricing.

Focusing on the GP-led space, Reach Capital surveys indicate that 42% of respondents would only consider continuation vehicles for companies with EBITDA levels of €10–20 million, significantly narrowing the competitive landscape. Additionally, 63% of surveyed managers report investing in small continuation vehicles only opportunistically, with just 33% of GPs incorporating them into their core strategy. These trends underscore the less competitive nature of the lower mid-market within the secondaries space.

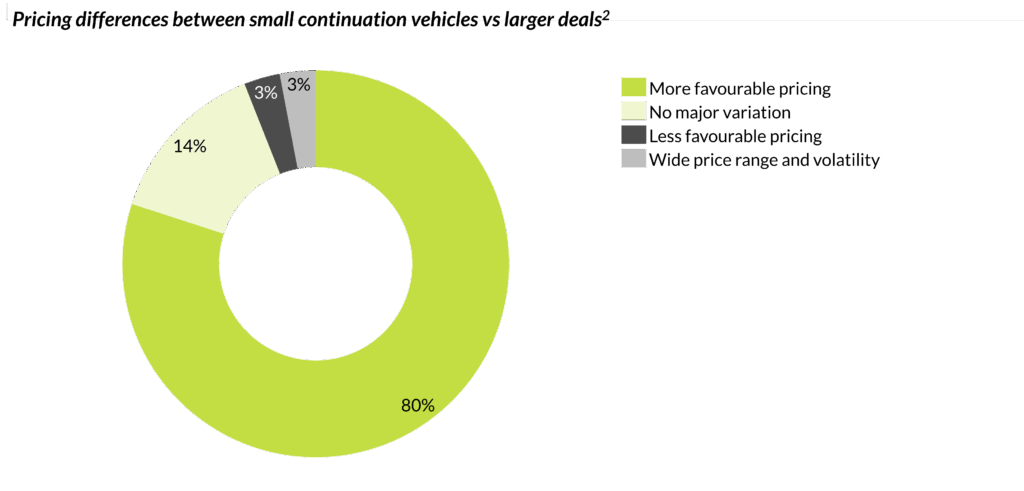

This lower level of competition translates into more favourable pricing, with 80% of managers expecting better terms in small continuation vehicles compared with larger deals, according to Reach Capital’s survey.

In conclusion, the secondary market has evolved from a niche segment into a permanent and essential solution to liquidity challenges in private markets. Beyond providing flexibility for both GPs and LPs, secondaries give investors access to proven assets with greater visibility, shorter durations, and attractive return potential.

Reflecting broader trends in private equity, the lower end of the market benefits from reduced competition, resulting in more favourable pricing for both GP-led and LP-led transactions. The secondary market is no longer just a liquidity tool—it has become a core lever for growth, alignment, and portfolio optimization in private capital.

Notes

Note 1: Sourced from Evercore Private Capital Advisory

Note 2: Sourced from Reach Capital’s report “Continuation Funds: How long can you go?”