While performance remains a central question in private equity, understanding the underlying growth and evolving investment behaviour is equally vital to grasp market dynamics.

The private equity market in Europe has experienced a clear upward trajectory over the past decade, with deal values increasing steadily year over year. However, since 2018, the pace of this growth has slowed, declining from an average annual increase of 13% (2014–2018) to 7% in the period from 2018 to 2023. However, 2024 marks a year with a notable recovery, with total deal value reaching €595BN, +36% of theprevious year’s volume.

When comparing the three-year averages of 2018–2020 and 2021–2023, all the regions where Qualitas Funds is active show positive growth. Italy, the UK and Ireland, and the Nordics stand out with the most substantial increases. This broad-based growth highlights not only the resilience of the European private equity market but also the strong performance of key investment regions.

Alongside this overall growth, we can observe a series of emerging trends that are reshaping the structure of private equity activity across Europe. One of the most notable shifts is the rise of add-ons and growth capital deals at the expense of traditional buyouts (LBOs).

When comparing the 2014–2018 and 2019–2023 periods, both add-ons and private equity growth/expansion deals have shown remarkable momentum. In absolute terms, add-on deals grew by c.89%, while private equity growth/expansion deals surged by c.122% across Europe. This increase is also reflected in their relative weight within overall private equity activity, where the share of add-ons rose by 7.7%, and private equity growth/expansion gained 3.6 points.

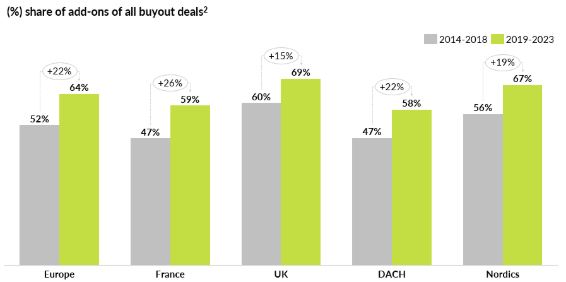

This trend is further confirmed when looking at the share of add-ons within total buyout deals. Across Europe, the proportion of buyouts structured as add-ons increased from 52% in 2014–2018 to 64% in 2019–2023. The shift reflects the growing adoption of buy-&-build strategies, as firms seek to create value by acquiring and integrating smaller targets rather than relying on large standalone transactions.

While private equity strategies have evolved in recent years, sector preferences have remained relatively stable, with clear signs of consolidation around core verticals. B2B and IT have long been leading sectors in European private equity, and recent data confirms that their dominance has only strengthened.

Looking at the sector composition between the 2018–2020 and 2021–2023 periods, B2B, B2C and IT continue to represent the bulk of deal activity. B2B increased its share from 30% to 33%, IT remained stable at 19%, while B2C declined to 20% from 23%. This consistency signals strong investor confidence in these segments, which continue to offer scalable business models and long-term strategic value.

Despite this apparent stability, underlying growth tells a more nuanced story. B2B grew by 3% in relative share and by 57% in absolute deal value, likely benefiting from a gradual shift away from B2C, which declined by 2.5 points, amid growing concerns around consumer demand volatility and macroeconomic uncertainty. Meanwhile, IT expanded moderately in share (+0.5%) but strongly in value (+46.6%). This growth reflects the sector’s continued relevance in driving digital transformation, automation, and operational efficiency across industries.

Energy also stands out, with 1.2 points of share growth and nearly 70% expansion in deal value. This surge reflects the momentum behind renewable energy, infrastructure, and sustainability-driven investment themes. The trend is driven by Europe’s push for energy independence, strong policy support, and the declining cost of renewables, positioning the energy sector as both an ESG priority and a long-term value opportunity for private equity.

Healthcare is the sector that has seen the biggest relative decline after B2C (-1.1%). However, this drop is better understood as a correction following an exceptional increase in relative weight during the pandemic. In 2020, while most sectors saw significant declines due to COVID-19 disruptions, healthcare remained resilient, causing its relative share to spike. As the broader market rebounded in 2021 and 2022 healthcare’s weight normalized.

In summary, the European private equity market has demonstrated solid resilience and adaptability, even amid macroeconomic volatility. The ongoing rise of add-on strategies, the consolidation around B2B and IT, and the growing importance of sectors such as energy, signal a market increasingly shaped by structural trends. Looking ahead, continued emphasis on digitalisation, sustainability, and operational scalability is likely to drive future investment strategies.

Notes

Note 1: Italy range is 2019-2023

Note 2: Sourced from Pitchbook and Qualitas Funds’ analysis