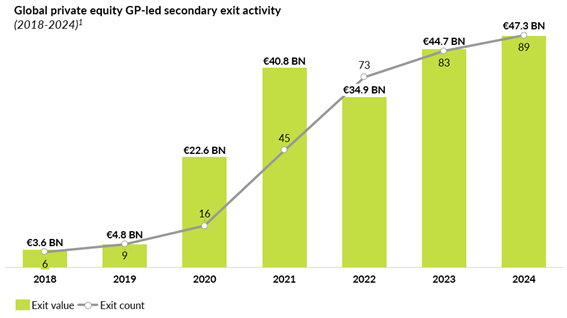

The use of these facilities can be increasingly relevant to the private equity industry, as the GP-led secondary exit activity has seen significant growth. GP-led secondaries refer to secondary market transactions in which the GP takes the lead in restructuring or managing the fund’s assets to provide liquidity to existing investors and maximize value. These transactions can take several forms, including continuation vehicles, which constitute a substantial portion of the total exit activity.

A continuation vehicle (CV) is a new investment fund alternative used by General Partners (GPs) to extend the holding period of one or more portfolio companies. Instead of selling these assets to third parties, the GP transfers them into a separate vehicle, allowing existing investors to recover their investment or reinvest in the new fund.

Continuation vehicles offer a range of advantages that explain their increasing popularity. One of the key benefits is the liquidity they provide to the existing fund investors, who receive distributions when the assets are bought by the continuation funds. Another significant advantage of continuation vehicles is their ability to support high-growth investments, allowing GPs to increase their exposure to the winners in their portfolio. By transferring high-performing assets into a continuation vehicle, GPs can secure additional capital to drive further growth in these promising investments, providing flexibility to extend the holding period for exceptional assets that require more time to reach their full value creation potential. These vehicles also open opportunities to attract secondary buyers. Investors in the secondary market are often interested in mature assets with a clear track record, making these vehicles an appealing proposition. By engaging this pool of secondary capital, GPs can diversify their investor base.

However, CVs also have drawbacks. One of the main problems is the potential conflict of interest that arises during the valuation process. As GPs represent both the selling side and the buying side, ensuring a fair price for both existing and new investors can be challenging. Another issue is that assets in CVs may move outside the manager’s original strategic focus in terms of company size, as companies in continuation vehicles typically grow beyond the manager’s typical investment sweet spot. Besides, managing both funds can increase the GPs’ operational complexity because of the need to oversee more entities simultaneously.

Taking into account the previous considerations, we can determine when it makes sense to raise a CV and when it might be better to explore other options. A CV is ideal when there is a clear, long-term growth path for the assets, such as in a fragmented market with potential for “buy and build” strategies or assets growing at a fast pace. Furthermore, having high minimum returns both in terms of MoC and IRR are a strong indicator that the assets have the potential to generate solid returns over the expected holding period. Besides, the management team’s track record is an important element to bear in mind. If the team has a proven history of successfully driving value and executing growth strategies, it can make sense to continue managing the investment through a CV.

However, a CV may not be beneficial for new investors if the growth path for the assets is uncertain or if there is a pressing need for liquidity from the current investors. Investors in continuation vehicles should also be careful if previous M&A processes have failed or if the asset’s valuation when rolled into the vehicle is above market levels. Furthermore, when the expected returns are purely based on IRR, without a clear path to significant value creation in terms of MoC for a 3-5 year holding period, it may be better to consider other strategies instead of raising a continuation vehicle.

NAV lending stands out as the most suitable alternative to raising a continuation vehicle, especially for funds with seeded portfolios and shorter-term capital requirements. It enables funds to secure financing without the need to resort to the structural complexity and extended timelines associated with a continuation vehicle. This approach is particularly advantageous when the fund requires immediate capital for follow-on investments, operational needs or taking advantage of urgent opportunities. Additionally, NAV lending provides an efficient financing mechanism, as it allows existing fund investors to continue capitalizing on the growth trajectory of the fund’s assets and avoids the conflict of interest of selling an asset from one vehicle and buying it from another one managed by the same GP.

Nevertheless, if a fund has identified a clear value creation case for its assets, then raising a continuation vehicle could be the best alternative. In doing so, fund managers can apply leverage to the structure by using a continuation vehicle loan. With this financing, GPs can unlock new opportunities to enhance value for investors. By investing the capital at a cost of equity but borrowing at a lower (debt-like) cost of capital, GPs can obtain better returns while maintaining a manageable risk profile, especially if the assets are already generating stable cash flow.

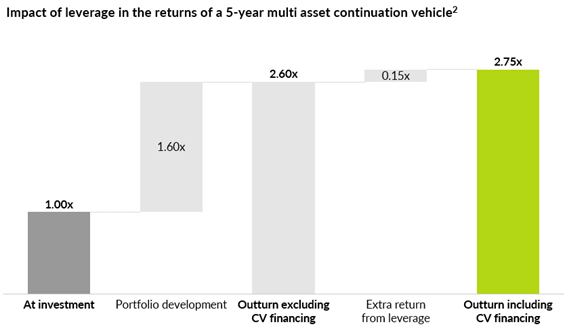

To exemplify our argument, we present a case study of how a fund can use CV loans to finance the new vehicle. Consider a growth private equity firm that invests in the B2C consumer and technology sectors, who has decided to create a c.€540MM CV to hold three of the portfolio companies from its second fund. The value of the CV’s assets is €180MM in total and an additional €360MM will also be invested to fund new investments and support the growth initiatives.

To carry out the transaction, the fund is exploring the use of a multi-asset continuation vehicle loan of €60MM as a substitute for some of the additional equity. This would enable them to achieve better returns by investing the capital at cost of equity but borrowing at a lower cost of capital.

If the fund’s expectations are accurate, the CV’s overall outturn will be 2.6x gross MoC. However, with the incorporation of the loan, the gross MoC increases to 2.75x, materialising the enhanced returns of the additional financing.

In conclusion, we observe that the number of GP-led secondaries is rising, especially the use of continuation vehicles. To successfully raise a CV, there must be a clear and long-term value accretive path for the assets, along with a reasonable entry price. If these conditions are not met, NAV financing could be a more suitable alternative to continue supporting the growth of the assets. However, if a CV is launched, fund finance tools such as multi-asset continuation vehicle loans can be utilised to further enhance the vehicles’ returns.

Notes

Note 1: Source: Pitchbook.

Note 2: Qualitas Funds’ scenario analysis of incremental returns resulting from the use of a multi-asset continuation fund loan.